Supporting UK consumers with clear, FCA-aligned financial education

Investment Goals

Choose a financial goal to see practical guidance on how to get started.

How to build up an emergency fund

Produce a list of costs that you run up every month.

Calculate how much you spend each month.

Decide how long a period you would like to have covered by this emergency fund.

Decide how long you want this fund to last because it will govern your investment decision – 1 month or 2 years. This is important because the effect of inflation must be considered. There is no point in saving £1,000 for 2 years on deposit as it will not buy the same amount of emergency cover at the end of the period.

Do you want this money to be available immediately? If not then alter your time period.

If the fund is to last 2 years consider how much risk do you want to take. Normally the greater risk, the greater the potential return.

In general, emergency money needs to be:

- Instantly available

- Generating a return which is more than inflation

Possible ideas

- ISA: all ISAs are instant access and can be invested in a wide variety of investments with varying levels of volatility.

- Capital risk free: bank accounts.

- Low risk of falling prices: certain fixed income bond funds. Access to these is through investment platforms or financial advisers.

Pay off student debt or help with house deposit

This is a thorny issue: student debt versus deposit for a mortgage for a family member.

Students have come to view tuition fees as yet another tax. The latest version of fees is taking an extra 9% of a student’s income when they start work and could result in them paying a marginal tax rate of 51%. They could be paying this tax for 40 years.

Reducing the weight of this debt for your child would allow them financial independence and the headspace to make decisions for their long-term future and wellbeing.

Paying the cost of tuition fees and living costs up front may well suit a student better than help with a deposit for a house.

Inheritance tax (IHT). Now that pensions are included in an estate at death, some grandparents have opted to help grandchildren with tuition fees and house deposits which can be considered as potentially exempt transfers and IHT free should they live for more than 7 years. Also gifts out of excess income could help.

The choice of helping the next generation to avoid a debt trap or have an easier path into house ownership is a difficult decision and is very dependent on the different financial positions of the members of the family.

Save for a house deposit

There is no time like the present to start.

Bear in mind that once you have saved for the deposit you will be putting aside an amount of money every year for the mortgage.

Don’t forget the cost of stamp duty and lawyer’s and surveyor’s fees.

Inflation is a killer for cash savings. The buying power of your £ falls significantly in periods of high inflation. If you will be saving for more than 2 years you need to make sure that your savings are protected from inflation.

Decide how much you can afford to put by every week.

Decide how much you need to buy a house in your area. This depends on two things: the price of the home and the type of mortgage you take out.

Deposits typically are a minimum of 5% of the asking price but most first-time buyers put down 10–20%.

Keep an emergency fund in cash. This may well be in a cash ISA if you are just starting out. Choose an account with a suitable interest rate which may well not be with your bank. Internet searches on comparison websites will help you as rates change regularly.

For the first time buyer an option could be a Lifetime ISA which gives you a 25% government boost each year. However, this ISA comes with restrictions on what you can buy and penalties if you cash it in.

For those with a time horizon of more than 2 years you could invest directly into a cautious fixed income fund in a stocks and shares ISA depending on your individual financial situation in order to keep up with inflation.

For those who are more adventurous, managing their own investments in a stocks and shares ISA on an investing platform might be more rewarding. More risk could mean more reward. Investments with low volatility and fees are also important.

Save for a car or holiday

A car might be one of the first big ticket items that you are likely to buy.

Saving for a car is likely to be similar to saving for a short-term emergency fund.

Work out your monthly outgoings – e.g., rent, commute, living expenses.

Work out your pay / income after tax every month.

Place any extra at the end of the month into a high interest account.

These accounts vary every month and comparison websites can be useful to find one which will pay you more than your bank. If you think that it will take you a year or so to save up enough then you could choose a fixed income stocks and shares ISA which might give you more than a cash ISA.

Save for a wedding

Plan everything with military precision beforehand to give yourself the best chance of the day you both hoped for, and then just relax and let it happen. This would include looking after the money that you have or will save and how long you are giving yourself to save. Some say the average cost of a wedding is around £28,000 depending on your choice of venue and numbers.

What to do with your money depends on inflation and current interest rates. The options are:

- Capital risk free in a bank’s savings account or cash ISA.

- Capital risk free for 1/2/3 years in a fixed term deposit at your bank but it will be locked up for a certain period.

- Stocks and shares ISA – higher risk but potentially higher reward and much more investment choice.

Wedding Packages

Booking a venue that offers wedding packages can be a cost-effective option as it often includes catering and drinks in addition to the venue hire. The average cost of this kind of package starts from around £6,000 for a winter mid-week wedding date and increases to £14,000 on average for a summer Saturday wedding. Those that provided a “typical” wedding package price averaged at £9,000.

Dry Hire Venue Costs

If you’re hiring your wedding venue on a ‘dry hire’ basis (i.e., bringing in all the caterers, decor and bar yourself) then your prices will look a little different. The average cost for booking a dry hire wedding venue on Saturdays during the peak season in the UK is around £8,000. However, if you opt for off-peak mid-week dates, you can expect to spend approximately £4,000.

Cost-Per-Head Wedding Packages

Wedding venues that charge couples on a per head basis often provide a comprehensive package that includes venue hire, food, a drinks package, and attentive staffing. For 2026, cost per head packages range from £85–£138, with an average median cost of £112 per person.

Depending on the marquee size and style, the national average “typical” cost is around £4,000 – and this is before the church/choir/celebrant (~£706), wedding planner, and staff.

How to invest a gift

Think about what your goals and time frame are, then invest.

How to pay off a credit card

A credit card can be very useful but you do need to pay it off in full each month. Otherwise the credit card company will charge you between 25% and 35% per annum. For example, if you purchase an item for £100, in a year it will cost you around another £25. They make it complicated to work out because they get you to pay a minimum each month, but rest assured it is the most expensive way to borrow, apart from a loan shark!

In an ideal world you would not buy an item if you did not have the money. But if you have, the most important thing is to pay it off as quickly as possible. Try to scrimp and save to reduce the debt.

Look through your bank statement to identify what you need to live off. If you can, work with a friend to help you to minimise any outgoings. Then:

- Hide your credit card so that you do not make it worse

- Try to pay for things using cash or a debit card wherever possible

- Delete any shopping apps and remove your saved card details on-line

- Unsubscribe from store marketing emails

- Make it difficult to impulse buy – try to sleep on a purchase

- Consider how many hours you need to work to pay for a purchase before buying it

- Pay more than the minimum monthly payment whenever possible, as this can significantly reduce both the repayment period and the total interest paid

- If you get tempted to merge the debt on your cards with a 0% balance transfer, ensure that you clear the balance before the promotional period ends

Hopefully by doing these things you be able to pay down the credit card debt quickly. Then check out how to build up an emergency fund so that you don’t in a pickle again.

How To…

Practical guides covering the essential skills for managing your money.

How to plan

As Winston Churchill famously said: “Those who fail to plan, plan to fail.”

- Review your spending pattern – compare income each month against your spending.

- Work out what you can save from your wages – set aside a regular amount to build up an emergency pot.

- Set up a regular standing order to top up your ISA when you get paid – even a small amount will build up over time.

- Pay off any high-interest credit card debt – the interest rate on borrowing varies; pay off the most expensive first.

- Define specific targets – e.g., build an emergency fund in 3 months, save for a nice holiday in 12 months.

- Measure progress to the goal – monitor growth monthly – review your regular amount.

- Ensure each stage is achievable – if not, adjust your budget to reflect changes in life.

- Be realistic with time frames – if not, adjust your goals.

How to save

If you are a spender, it’s not easy, therefore try to start with baby steps. If you can set aside something each week it is surprising how it builds up.

Start with a very small amount say £1 per day or £5 per week. Try to automate it with a standing order when you get your wages. The aim is to grow an emergency pot. It may help to give yourself a goal, for example save for a weekend away.

If your bank offers it, turn on the round-up feature or use an autosaving app. For example, spend £2.90 on a coffee and 10p is moved into a savings account.

Go through your bank statements to ensure that you need all your subscriptions or at least review them to see if you can improve them.

If you are a spender, try to sleep on it before buying an expensive item or discuss it with a friend before buying.

Do not store credit cards on websites to make it a little more difficult to spend.

Try to plan your spending so that you know where each pound goes.

If you have any credit card debt this must be your first goal to pay off. As the interest rate tends to be the highest.

How to invest

There are two main ways of increasing your cash: saving and investing. This is assuming that you already have an emergency pot.

In saving you are lending cash for example to a bank and they will give you interest. However, they are a business and need to make a profit. Therefore, they borrow your money and lend it out to someone who wants a mortgage, at a higher rate of interest. Therefore, you are not going to make a great return.

If you invest however, you have more say on where your cash is invested. There is the potential to get a higher return and the most popular way to invest is via a specialist fund manager to actively manage your money for you.

The active fund manager can invest into a range of sectors to diversify risk. They pool your money with other investors like you. The main sectors are fixed income and equities. Also, within these sectors there are many subsectors to again diversify risk. All funds have a theme, where their experts invest across the world.

You could invest into the subsectors yourself but initially it is safer to give an active fund manager the responsibility as they have a supporting team of analysts to invest on your behalf.

Fund managers now use AI to analyse the best companies within their sector to tactically select where to invest.

But remember with investing there is an element of risk, but investing in fixed income is much less risky than equities as the price bounces around less. If you combine different funds with different themes, you can build a strategic portfolio to diversify risk.

The returns you will receive from your portfolio will depend on which themes you chose. The difference between the price you pay and the price you sell for is either a capital gain or loss. Equities pay dividends and fixed income pays interest.

You should never invest more than you can afford to lose, which is why you should always invest into a fund. However, in a capitalist society the markets should bounce back up over time.

Good investing is finding the right mix of different types of investments that match your comfort with risk. This is called ‘asset allocation’, and it’s something you might want to get advice on from a regulated financial adviser, who would normally give you an initial consultation for free.

How to budget

A budget is simply a plan for your money. Start by listing all your income and regular outgoings each month.

Look for areas where you could reduce spending. Set aside a fixed amount for savings as soon as you get paid – treat it like a bill you must pay.

Many banking apps now include budgeting tools that categorise your spending automatically. Review your budget monthly and adjust as your circumstances change.

See our How to Plan section for a step-by-step approach to managing your finances.

How to use AI

The optimal way of searching with AI (a large language model) is to ask a clear question, giving relevant context and being specific about what you want back.

Use this simple structure:

- I want (goal)

- I am (context)

- My constraints are (X)

- Please give me (type of answer)

Example

I want to buy a low volatile UK fixed income IA strategic bond fund. There are a number of funds from the Authorised Corporate Director Valu-Trac. I am new to investing and therefore I want an active fund manager to tactically adjust the asset allocation for me. I would like to purchase the fund via Interactive Investor . The fund must have a Financial Express risk score of 20 or lower. Please recommend 3 options and explain the differences.

The FCA has also published guidance on using AI responsibly when researching investments.

Please use the following link to FE to search for funds in the strategic bond sector.

What Is…

Key financial concepts explained in plain English.

Fixed Income

Fixed income or fixed interest or bonds are investments where you lend money and receive an IOU. You lend money and you receive interest and your money back sometime in the future.

Bonds are popular with those who like the peace of mind that comes from knowing that you will receive regular interest for a fixed period.

Most income investors like bonds as it gives you a predictable income with lower volatility than equities.

By lending money to a company or a government you fix the interest (coupon) that you will receive for the life of the IOU.

The quality of each company or government is rated and therefore the lower quality companies will need to tempt the investor with a higher interest level.

For example, for lending to a supermarket you would receive a higher yield (interest) than the Bank of England.

Also, the longer the IOU before the investment is repaid, the higher the interest level. Recently Alphabet (Google) issued a 100-year bond to fund investment in AI. To tempt investors, they had to pay 6.125% in interest.

As the fixed income market is larger than the equity market, active fund managers use AI to search for the most profitable bond issues. As the fund manager is active, they tactically buy and sell bonds. Corporates issue a wide range of high yielding bonds with varying maturity lengths and with different levels of security.

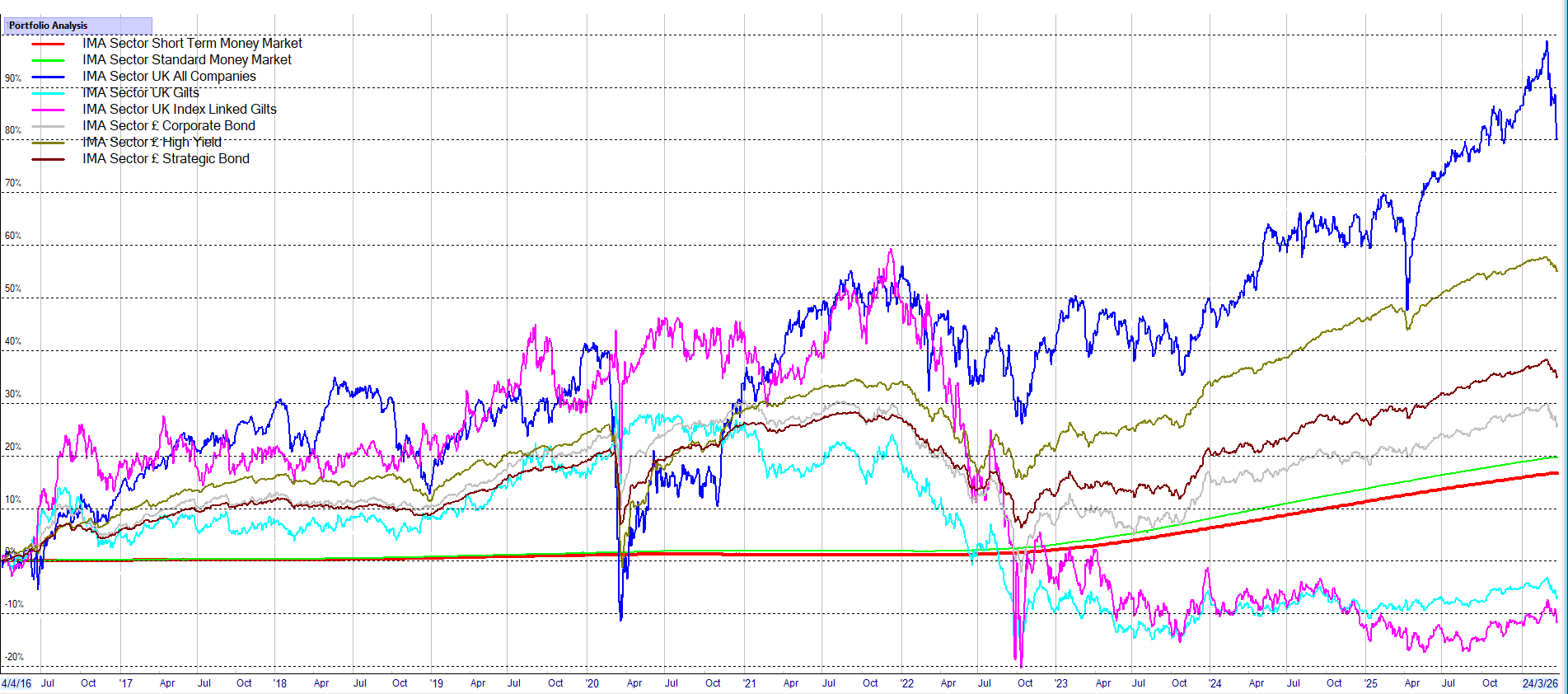

The following chart from Sharescope shows the Investment Association (IMA) fixed income sectors plotted against the IMA UK equity sector since 2016.

Equities

The terms equity, shares and stocks are all used to describe a tiny part of a company.

The company will hopefully grow its profits and your share will enjoy a portion of the increase in the company’s profits and be paid a dividend.

However, a company’s profits will not only be affected by its own strategy, but also by world events and therefore growth cannot be guaranteed. Unlike fixed income where there is more predictability and therefore lower volatility.

The most popular way of investing in the shares of a company is via a specialist fund manager. The fund manager typically uses AI to reduce down the number of companies and then meets the company to decide if investing is a good idea. They monitor the investment for you and if the company does not deliver, the fund manager sells and buys another company.

The equity fund manager typically invests in 30–100 individual companies within a theme to diversify risk. Also, each company normally invests in different sectors and countries.

Inflation

The easy explanation: if you buy 1 litre of milk for £1 today and in a year the price goes up to £1.04, the annual rate of inflation is 4%.

Another way of thinking about inflation: if the milk costs £1 in a year’s time but the size of the container shrinks down to 0.96L. Just like the size of some chocolate bars!

Even if inflation slows down, the price of milk will still go up each year. The rate of increase is due to inflation.

What causes inflation?

- Increasing costs – as we need to import oil and gas the cost of transporting materials into the UK increases, affecting manufacturers.

- Competition – when demand increases, like tickets to see your favourite music band, the cost goes up.

What is the impact of inflation?

If your wages are increasing by 3% per annum, but food and petrol prices are increasing at 4% per annum, then your wages are not keeping up with inflation and your household finances are being squeezed.

A less obvious effect is the impact on savings. If you keep spare cash in your current bank account getting no interest then you are losing 4% per annum.

How to protect savings from inflation

Cash savings offer little capital risk but also little return. But they do have inflation risk when the interest rate doesn’t keep up with the inflation rate.

This is where investing into fixed income can help. You could lend your cash to very large companies e.g., supermarkets and get a higher return (yield). Please see how to invest in fixed income.

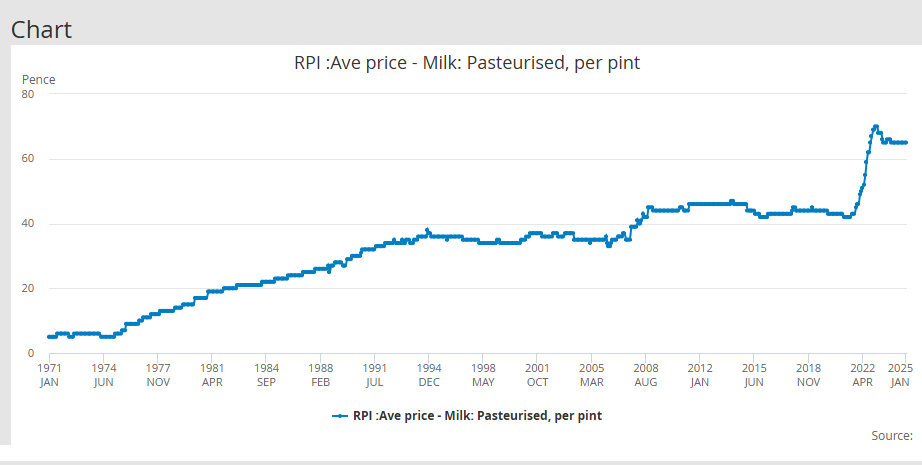

The following chart from the ONS shows how inflation has affected the price of milk since 1971:

Interest

If you lend money you would expect to receive some return. If you lend money, you would also hope to get it back.

It is the combination of potential risk and the length of time, that determines the level of interest.

If you lend to a bank you would expect to get it back. If you want the ability of getting it back quickly, as in a current account, you would not expect a high interest rate if any.

However, if you lend cash to a bank but are happy to lock it away for say 12 months, then you would expect to receive a higher interest rate.

You could also lend money to a company e.g., a supermarket. As there is the potential for the supermarket not to pay you back you would expect to get a higher interest rate than a bank.

For example, you can get a higher yield (interest) by investing in a wide range of very large companies. Active fixed income bond fund managers use AI to search out for companies that need money and tactically lend to them. The lower quality the company the higher yield (interest) it will need to pay to attract investors. To spread risk the fixed income bond fund manager tactically invests into up to 1000 companies just in case they do not pay back the investment.

Where to Invest

Understand the accounts and tools available to you.

ISA (Individual Savings Account)

An ISA is an Individual Savings Account. But it is more than that – you can shelter income, dividends and capital gains tax from saving / investing for life.

The government wants the public to look after themselves financially and currently allows an adult to invest up to £20,000 per financial year (starting 6th April each year) in total into a range of ISAs. For anyone under the age of 18, the limit is £9,000.

The best way of opening a stocks and shares ISA is by using a website often called a platform.

If you wish to merge your ISAs, choose a platform that is flexible. Some platforms allow you to take money out for emergencies but also to put it back in within the financial year without losing your allowance. Typically, you can take cash out within 2 weeks and there should not be any additional charges.

There are a number of ISAs each with varying features. The main ones are:

- The cash ISA which can only save in cash.

- The stocks and shares ISA which can hold cash but also fixed income and equities. You can blend them together using AI to build a strategic portfolio from funds to diversify risk.

Other types of ISAs

- Junior ISA – for someone under 18 years of age.

- Help to Buy ISA – closed to new investors.

- Lifetime ISA – designed to help people aged 18–40 save for their first home or retirement.

- Innovative Finance ISA – these allow you to invest into peer-to-peer loans.

There are rumours that these are being reviewed.

Platforms

The cheapest way to buy an ISA is through a website, often called a platform.

Platforms are regulated by the Financial Conduct Authority (FCA).

There are a wide range of platforms in the UK, each with varying features. As throughout your life you will need to monitor your financial investments including pensions / SIPPS, it would be sensible to choose a platform that will be able to support you during your life.

A good platform would have a wide range of accounts and also access to thousands of funds. You should be able to buy both fixed income and equity funds.

Each platform charges to look after your investments. There should not be an initial or exit charge but they need to charge for admin. They should also be ‘flexible’ to allow you take money out of an ISA and put it back within the same year.

The platform also enables you to buy and sell your investment funds. This charge may be included in the admin fee or separately charged.

The platform should also have an app to allow you to monitor your investments. It might also have some tools to analyse your portfolio.

If you wish to tidy up your investments you should be able to place them all on the same platform to help you monitor all your financial needs.

To help you find a platform, the analysts at Kepler Trust Intelligence have produced some research to help: Best ISA providers in 2026.

Also see Boring Money's guide to ISAs & Pensions.

News & Links

Useful articles and resources from across the web.